The drawdown in stock markets during the February 20 – March 23 period was severe and took most by surprise, given the rosy outlook that launched 2020. Credit is due to the Federal Reserve and the government for promptly acting and providing stimulus to the markets, to businesses and to consumers whose spending makes up 70% of the economy. While the COVID-19 recession is global and remains very real, Work from Home stocks including the much-discussed FAANGMi began to lead the U.S. markets higher in late March.

Through the summer and into the fall the markets rotated to include participation by more economically sensitive businesses. Economic expectations improved, bolstered by positive drug trials for COVID-19 vaccines. Smaller capitalization companies that had experienced more modest returns came alive in November with the returns of the Russell 2000 being the strongest on record. The outcome of the U.S. election and the prospect of a government divided between a Democratic President and a Republican Senate offered an outlook for subdued regulatory change that has been welcomed by the markets.

Inside the Numbers

As often occurs with an outlook for economic recovery and the exit from a recession, smaller capitalization and lower quality businesses outperformed. To highlight this, QSV examined our universe of stocks and sorted by those with positive and negative net income during 2019. Through December 8, 2020, companies in the Russell 2000 Index with negative net income have risen 32.6% in 2020; those with positive net income have risen only 3.7%.

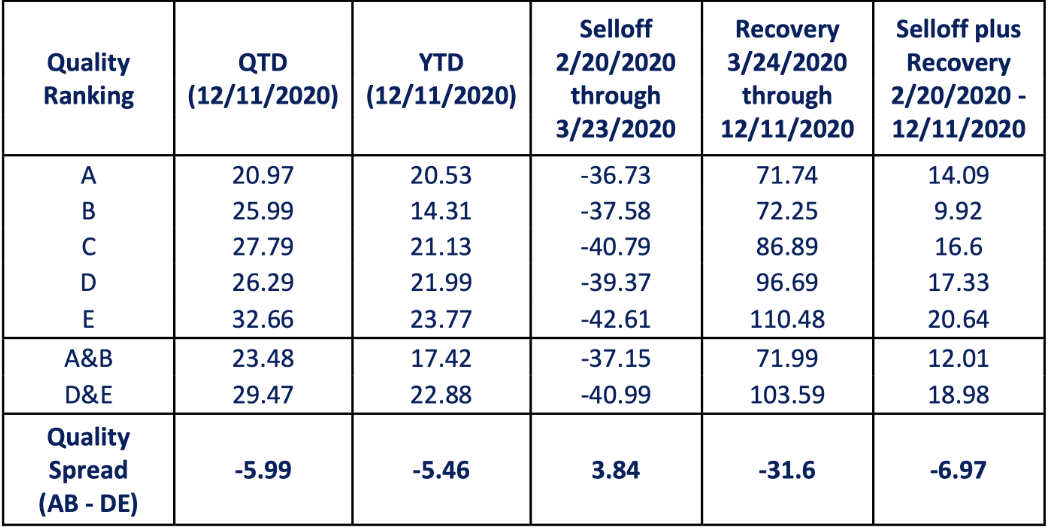

QSV is committed to investing in quality businesses, those we believe have durable competitive advantages, stable and growing returns on invested capital, low leverage, and stable and persistent earnings. After patiently waiting for the stocks of those businesses to be reasonably priced, we invest our clients’ and our own capital with the belief that the resulting portfolio will provide a smoother ride, participating well in rising markets while protecting capital in falling markets and delivering competitive, risk-adjusted returns over a full market cycle. QSV uses a proprietary ranking system for its universe of prospective holdings, with companies ranked in the top two (A and B) quintiles recognized as high quality and those in the bottom two (D and E) quintiles considered low quality. As shown below, high quality businesses did help protect investors, as anticipated, during the sharp selloff in February and March. Also as expected, lower quality stocks have soared more significantly in the recovery that has followed, creating a headwind for the performance of quality-biased investment strategies during 2020.

Looking solely at the smaller capitalization (under $3 billion) businesses within this universe, the disparity between high quality and low-quality concerns has been even more significant for the year-to-date 2020 period and during the recovery since March. This, too, is expected, as smaller companies often have more volatile earnings and more volatile stock performance, but it has stood as a strong detractor to the relative performance of quality-biased investment strategies.

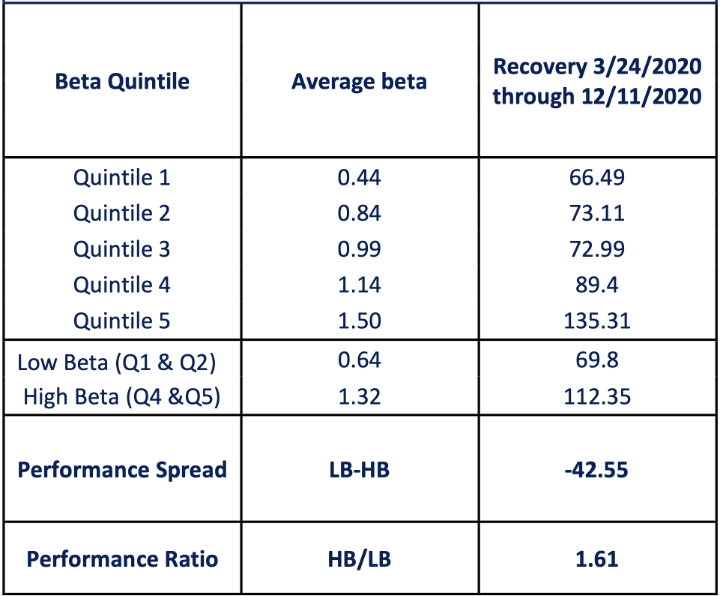

Performance headwinds for quality-biased strategies during 2020 can also be explained by equity beta, or how sensitive the stock price is to a change in the overall market. Using the full universe of prospective holdings that QSV monitors, we found that high beta outperformed low beta by 1.61 times during the recovery since March, with a return of 66.49% for the lowest beta quintile and a gain of 135.31% for the stocks in the highest beta quintile.ii

QSV has previously written a white paper, The Myth of High Beta, where we address the belief by some that high beta stocks are the answer to investors’ long-term investment success. We disagree, believing that low volatility stocks are better suited to deliver above-average returns over longer time frames. The QSV strategies and those of other quality-biased investors are generally characterized by lower than market levels of beta. Comparing the holdings in the QSV strategies from the March 23, 2020 market low to those of the Russell 3000, we found betas of .91 for QSV Quality Value Midcap, .88 for QSV Quality Value Smallcap and .89 for QSV Select Value strategy.

Outlook: Truckin’ into 2021

When considering the near-term outlook for QSV and other quality-biased investment strategies, we will again look to the Grateful Dead and borrow its lyrics: “Sometimes the lights all shinin’ on me; other times, I can barely see.”

The robust returns of 2020, particularly for the stocks of lower quality, more economically sensitive businesses, were built on an expectation of greater economic prosperity to come. Both lower income and higher income workers continue to feel impacts from the COVID economy; wages for higher income workers (those that propel much of consumer spending) fell in November during the very period that the Russell 2000 Index was recording record gains.iii Corporate debt has climbed and there are a rising number of “zombie companies” or those that are in debt such that any cash generated is being used to pay off the interest on the debt. While the stimulus provided by the government in 2020 was necessary to prevent more immediate, profound destruction, it has propped up lower quality businesses with limited or no earnings and supported frothy stock returns in areas of the market that offer little in the way of real business performance. Adding to worries is that the aforementioned divided government and its prospects for subdued regulatory changes remains a question mark. The upcoming runoffs in the Georgia Senate could result in a “Blue Wave,” with risks of unwinding the deregulation and tax cuts that resulted under the Trump administration.

The New Year is upon us and opportunities and risks abound. Focusing on quality businesses, where there is transparency (a “shinin’ light”) into the competitive advantages and drivers of business performance, is essential to constructing portfolios that will both manage risks and deliver returns in the future.

About QSV Equity Investors, LLC

QSV Equity Investors, LLC is an employee-owned asset management firm that invests alongside its clients in high conviction portfolios of quality small and mid-capitalization businesses. QSV manages these portfolios of publicly traded companies for individuals, family offices and institutions. Based in Oakbrook Terrace, Illinois, QSV was founded in 2016 by Jeff Kautz and Randy Hughes, investment professionals who previously held senior roles at Perkins Investment Management and have invested together for over 20 years. For more details on the specific performance and characteristics of the QSV strategies, including a fully GIPS compliant presentation, please contact Dave Mertens at dmertens@ballastequity.com.

i Facebook (NASDAQ: FB), Amazon (NASDAQ: AMZN), Netflix (NASDAQ: NFLX), Alphabet (NASDAQ:

GOOG, NASDAQ: GOOGL) and Microsoft (NASDAQ: MSFT)

ii Beta was calculated using a three-year trailing Beta versus the Russell 3000 as of March 18, 2020 so as to not reflect performance since that date.

iii Heer, John (December 3, 2020) Analysis: Assessing the True Strength of U.S. Consumers’ Finances (morningconsult.com)

To borrow heavily from Jerry Garcia and Bob Weir of the Grateful Dead, what a long, strange trip 2020 has been. After beginning the year with great expectations (remember images like the one below?) and with the strong market returns of 2019 vivid in the minds of investors, the world faced the reality of a global pandemic that shocked the markets in February and March.

AP Photo/Mark Lennihan

The drawdown in stock markets during the February 20 – March 23 period was severe and took most by surprise, given the rosy outlook that launched 2020. Credit is due to the Federal Reserve and the government for promptly acting and providing stimulus to the markets, to businesses and to consumers whose spending makes up 70% of the economy. While the COVID-19 recession is global and remains very real, Work from Home stocks including the much-discussed FAANGMi began to lead the U.S. markets higher in late March.

Through the summer and into the fall the markets rotated to include participation by more economically sensitive businesses. Economic expectations improved, bolstered by positive drug trials for COVID-19 vaccines. Smaller capitalization companies that had experienced more modest returns came alive in November with the returns of the Russell 2000 being the strongest on record. The outcome of the U.S. election and the prospect of a government divided between a Democratic President and a Republican Senate offered an outlook for subdued regulatory change that has been welcomed by the markets.

Inside the Numbers

As often occurs with an outlook for economic recovery and the exit from a recession, smaller capitalization and lower quality businesses outperformed. To highlight this, QSV examined our universe of stocks and sorted by those with positive and negative net income during 2019. Through December 8, 2020, companies in the Russell 2000 Index with negative net income have risen 32.6% in 2020; those with positive net income have risen only 3.7%.

QSV is committed to investing in quality businesses, those we believe have durable competitive advantages, stable and growing returns on invested capital, low leverage, and stable and persistent earnings. After patiently waiting for the stocks of those businesses to be reasonably priced, we invest our clients’ and our own capital with the belief that the resulting portfolio will provide a smoother ride, participating well in rising markets while protecting capital in falling markets and delivering competitive, risk-adjusted returns over a full market cycle. QSV uses a proprietary ranking system for its universe of prospective holdings, with companies ranked in the top two (A and B) quintiles recognized as high quality and those in the bottom two (D and E) quintiles considered low quality. As shown below, high quality businesses did help protect investors, as anticipated, during the sharp selloff in February and March. Also as expected, lower quality stocks have soared more significantly in the recovery that has followed, creating a headwind for the performance of quality-biased investment strategies during 2020.

Looking solely at the smaller capitalization (under $3 billion) businesses within this universe, the disparity between high quality and low-quality concerns has been even more significant for the year-to-date 2020 period and during the recovery since March. This, too, is expected, as smaller companies often have more volatile earnings and more volatile stock performance, but it has stood as a strong detractor to the relative performance of quality-biased investment strategies.

Performance headwinds for quality-biased strategies during 2020 can also be explained by equity beta, or how sensitive the stock price is to a change in the overall market. Using the full universe of prospective holdings that QSV monitors, we found that high beta outperformed low beta by 1.61 times during the recovery since March, with a return of 66.49% for the lowest beta quintile and a gain of 135.31% for the stocks in the highest beta quintile.ii

QSV has previously written a white paper, The Myth of High Beta, where we address the belief by some that high beta stocks are the answer to investors’ long-term investment success. We disagree, believing that low volatility stocks are better suited to deliver above-average returns over longer time frames. The QSV strategies and those of other quality-biased investors are generally characterized by lower than market levels of beta. Comparing the holdings in the QSV strategies from the March 23, 2020 market low to those of the Russell 3000, we found betas of .91 for QSV Quality Value Midcap, .88 for QSV Quality Value Smallcap and .89 for QSV Select Value strategy.

Outlook: Truckin’ into 2021

When considering the near-term outlook for QSV and other quality-biased investment strategies, we will again look to the Grateful Dead and borrow its lyrics: “Sometimes the lights all shinin’ on me; other times, I can barely see.”

The robust returns of 2020, particularly for the stocks of lower quality, more economically sensitive businesses, were built on an expectation of greater economic prosperity to come. Both lower income and higher income workers continue to feel impacts from the COVID economy; wages for higher income workers (those that propel much of consumer spending) fell in November during the very period that the Russell 2000 Index was recording record gains.iii Corporate debt has climbed and there are a rising number of “zombie companies” or those that are in debt such that any cash generated is being used to pay off the interest on the debt. While the stimulus provided by the government in 2020 was necessary to prevent more immediate, profound destruction, it has propped up lower quality businesses with limited or no earnings and supported frothy stock returns in areas of the market that offer little in the way of real business performance. Adding to worries is that the aforementioned divided government and its prospects for subdued regulatory changes remains a question mark. The upcoming runoffs in the Georgia Senate could result in a “Blue Wave,” with risks of unwinding the deregulation and tax cuts that resulted under the Trump administration.

The New Year is upon us and opportunities and risks abound. Focusing on quality businesses, where there is transparency (a “shinin’ light”) into the competitive advantages and drivers of business performance, is essential to constructing portfolios that will both manage risks and deliver returns in the future.

About QSV Equity Investors, LLC

QSV Equity Investors, LLC is an employee-owned asset management firm that invests alongside its clients in high conviction portfolios of quality small and mid-capitalization businesses. QSV manages these portfolios of publicly traded companies for individuals, family offices and institutions. Based in Oakbrook Terrace, Illinois, QSV was founded in 2016 by Jeff Kautz and Randy Hughes, investment professionals who previously held senior roles at Perkins Investment Management and have invested together for over 20 years. For more details on the specific performance and characteristics of the QSV strategies, including a fully GIPS compliant presentation, please contact Dave Mertens at dmertens@ballastequity.com.

i Facebook (NASDAQ: FB), Amazon (NASDAQ: AMZN), Netflix (NASDAQ: NFLX), Alphabet (NASDAQ:

GOOG, NASDAQ: GOOGL) and Microsoft (NASDAQ: MSFT)

ii Beta was calculated using a three-year trailing Beta versus the Russell 3000 as of March 18, 2020 so as to not reflect performance since that date.

iii Heer, John (December 3, 2020) Analysis: Assessing the True Strength of U.S. Consumers’ Finances (morningconsult.com)