Q2 2024 Commentary

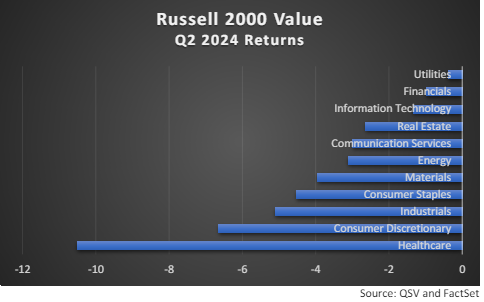

No one needs another investment commentary noting the divergence of Nvidia and the “Magnificent 7” stocks’ performance with that of the broader market, but it is hard to live through a quarter like Q2 2024 without that on our minds. This compact group of companies has contributed more than 60% of the returns of the index in 2024 and, when the returns of the capitalization weighted S&P 500 are compared to an equally weighted S&P 500, there is a 10% difference in favor of the cap weighted benchmark. While this dynamic plays out, investors have paid little attention to the pond QSV fishes in, small and mid-cap equities, where the returns were quite different, and negative during the quarter. Each sector of the Russell 2000 Value index delivered losses in Q2, with Utilities (supported by the prospects for data centers for the AI revolution?) only slightly in negative territory and Healthcare, where QSV finds an ample supply of quality businesses, suffering losses of more than 10%. Returns for mid-cap indexes were in similar,

negative, territory.

More information including since-inception performance for each QSV strategy may be found at www.qsvequity.com.

QSV Strategy Quarterly Performance

QSV Small Cap returned -3.76% and -3.84%, gross and net of fees, respectively, lagging the Russell 2000 Value Index return of -3.64% and the Russell 2000 Index return of -3.28%. Security selection in Healthcare helped performance, while an overweight in the sector detracted. Selection in Real Estate also aided performance. Selection in Industrials and Financials businesses detracted from returns.

QSV Small Cap Top Contributors

Napco Security Technologies Inc. (NSSC) shares rose nearly 30% supported by strong growth in revenues and gross margins in its business units. NSSC is a global provider and manufacturer of high-tech security products, including access control systems, door-locking products, intrusion and fire alarm systems and video surveillance products. The company is focused on doubling revenue within its recurring, high-margin Services business in the next 2-3 years and currently produces returns on invested capital of 17% while selling at a discount to our measure of intrinsic value.

Hawkins Inc. (HWKN), rose more than 18%, contributing to performance. HWKN is a leading provider of chemicals and ingredients sold through its industrial, water treatment and health and nutrition segments. The company has benefitted from fast growth in its high margin water treatment business which is expected to drive higher earnings and free cash flow growth as it represents a larger portion of the firm’s overall revenues. HWKN produces returns on invested capital of 13%.

QSV Small Cap Top Detractors

Shares of clinical research organization Fortrea Holdings (FTRE) dropped more than 40% during the quarter as the company fell short of analysts’ estimates of revenues and earnings and the company lowered its outlook. The company, spun out of LabCorp (LH) in 2023, benefits from offering tools and testing to the biotechnology and pharmaceutical industries that are highly scripted in law, regulation, and practice. QSV believes that it is not uncommon for a company to struggle initially post-spinoff and has confidence in the long-term outlook for FTRE. As a result, we added to our position on weakness in the share price.

Alamo Group (ALG) shares declined during the quarter as a five-week strike in one of its plants is expected to impact the quarter’s financial results. The manufacturer of agricultural and vegetation maintenance equipment settled the strike with a five-year contract that should remove the risk of labor disruption for some time. ALG operates as forty global brands in two key divisions: industrial equipment and vegetation management equipment. The company benefits from an extensive dealer network and leading market share. Sixty percent of its revenues come from state and municipal government contracts.

QSV Small Cap Portfolio Activity

Shares of Forward Air (FWRD) were sold after the company added debt for its Omni Logistics acquisition and, in our view, could not clearly define the mission for the combined business. PubMatic (PUBM) and Shutterstock (SSTK) were each sold for valuation reasons. Scotts Miracle-Gro (SMG) was sold as they continued to struggle with the exposure to the cannabis industry and the addition of debt, reducing our estimate of the company’s intrinsic value. Proceeds were invested in existing holdings as well as new holding Catalyst Pharmaceuticals(CPRX), a biopharmaceutical company focused on developing therapies for people with rare, debilitating neuromuscular and neurological diseases.

QSV Mid Cap returned -5.15% and -5.38%, gross and net of fees for the quarter, trailing the -3.40% return of the Russell Mid Cap Value Index and the Russell Mid Cap Index return of -3.35%. Security selection in Consumer Staples companies helped performance, as did company selection and an overweight to Information Technology companies. Selection in Financials detracted as did selection and an overweight to Healthcare.

QSV Mid Cap Top Contributors

Monolithic Power SystemsInc. (MPWR) was the leading contributor to performance in the quarter as the company delivered strong earnings growth and benefitted from the outlook for AI-related tailwinds. MPWR is a global provider of high-performance, semiconductor-based power solutions. As a “fabless” company – one that does not manufacture the chips used in its products – MPWR has profited from devoting more resources to chip design rather than capital expenditures, resulting in greater free cash flows, higher margins, and returns on invested capital of 22%.

Teradyne Inc. (TER), a provider of semiconductor chip testing equipment, also contributed to performance during the quarter as it beat earnings estimates and affirmed guidance. AI-related opportunities are contributing to current growth and an enhanced outlook while the company’s exposure to mobility produces headwinds due to lower demand. TER produces returns on invested capital of 26% and sells below our estimate of intrinsic value.

QSV Mid Cap Top Detractors

Fortrea Holdings (FTRE) was the leading detractor to performance during the quarter and is discussed above.

Lincoln Electric Holdings (LECO) detracted from performance during the quarter as the company saw softness in its quarterly revenues and lowered its full year earnings guidance. We see these as short-term issues for LECO, a trusted name in welding, cutting, and brazing products, with a leading global market share. While still in the commercialization phase, LECO is developing an EV charger business that represents an additional growth opportunity for the business. The company has raised its dividend for twenty-two years and produces returns on invested capital of 21%.

QSV Mid Cap Portfolio Activity

There were no total sales or purchases of positions during the quarter. QSV did add to its position in the clinical research organization Fortrea Holdings (FTRE) on weakness in its share price and made other trims and additions based upon valuation and our convictions in the fundamentals of the businesses.

QSV Select returned -4.40% and -4.62%, gross and net of fees, lagging the returns of the Russell 2500 Value and Russell 2500 Indexes of -4.31% and -4.27%, respectively. Select is a high conviction strategy that holds QSV’s best ideas from our Small Cap and Mid Cap strategies. Security selection was positive in Industrials. Selection and an overweight in Information Technology and Consumer Discretionary holdings also aided performance. Selection detracted from returns in Financials and Healthcare holdings.

QSV Select Top Contributors

Napco Security Technologies Inc. (NSSC) was the leading contributor to performance during the quarter and is discussed above.

Tyler Technologies Inc. (TYL) rose as its transition to Software as a Service, subscription revenues and earnings increased. TYL is the largest provider of enterprise software products focused solely on the public sector, with a focus on local governments where high switching costs stand as Tyler’s competitive advantage. The company has a 98% customer retention rate and incremental margins in its subscription business of over 70%. We continue to believe that TYL will benefit from increased government spending on infrastructure.

QSV Select Top Detractors

Fortrea Holdings (FTRE) was the leading detractor to performance of QSV Select during the quarter and is discussed above.

Vestis Corporation (VSTS) detracted from performance during the quarter. Formerly a division of Aramark, VSTS provides uniform services and workplace supplies to North American Customers ranging from small businesses to Fortune 500 companies. Business performance has been impacted by client retention dropping because of off-cycle price increases and sub-par results from the company’s sales team. We believe the company’s focus on improved service and sales productivity will get this performance back on track.

QSV Select Portfolio Activity

Limited trading was done in QSV Select during the quarter, with trims and additions made to address valuations and quality upgrades.

Our Focus on the Long Term

We believe that mid-year reflection is appropriate for investors including a close look at asset allocation. With the concentration of returns to-date in large cap equities, and specifically in a handful of companies, many portfolios are tilted in favor of those holdings. Unintended bets may exist where investors in both passive and active funds have stakes in the Magnificent 7 companies that have increased in size. Markets could be “different this time” but if the outperformance of the S&P 500 over the smaller companies in the Russell 2000 persists throughout 2024 it will cap a four consecutive year period of such outperformance, something that has not occurred since 1995-1998. Small and mid-cap value equities excelled in the years that followed that, while investors in large cap stocks endured the “lost decade” of returns. Compelling valuations currently exist in small and mid-cap businesses. Coupled with the possibility of lower inflation, lower interest rates, and potential tailwinds from deglobalization, we see a convincing case for allocating to quality small and mid-cap companies.

Disclaimer:

Returns are for the respective composites of QSV Equity Investors. Gross returns are calculated net of trading fees. Net returns are calculated net of trading fees and net of the firm’s management fee. All dividends are assumed to be reinvested. The returns of the QSV Small Cap strategy are compared to the historical performance of the Russell 2000 Indices as they are widely used benchmarks for small capitalization securities. The returns of the QSV Mid Cap strategy are compared to the historical performance of the Russell Midcap Indices as they are widely used benchmarks for mid capitalization securities. The returns of the QSV Select strategy are compared to the historical performance of the Russell 2500 Indices as they are widely used benchmarks for SMID capitalization securities. An investment with QSV Equity Investors should not be construed as an investment in a program that seeks to replicate, or correlate with, these indices. Market conditions vary between the QSV products and these indices. Furthermore, these indices do not include any transaction costs, management fees and other expenses, as do QSV products. Lastly, QSV may invest in securities and positions that are not included in these indices.

No client or potential client should assume that any information presented should be construed as personalized investment advice. Personalized investment advice can only be rendered after engagement of the firm for services, execution of the required documentation, and receipt of required disclosures. Investing carries risk of loss.

QSV Equity Investors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of the CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. To view a GIPS report, please visit www.qsvequity.com.

QSV Equity Investors, LLC is a registered investment advisor. For additional information about the firm and its professionals please visit the SEC’s website at www.adviserinfo.sec.gov.

Q2 2024 Commentary

No one needs another investment commentary noting the divergence of Nvidia and the “Magnificent 7” stocks’ performance with that of the broader market, but it is hard to live through a quarter like Q2 2024 without that on our minds. This compact group of companies has contributed more than 60% of the returns of the index in 2024 and, when the returns of the capitalization weighted S&P 500 are compared to an equally weighted S&P 500, there is a 10% difference in favor of the cap weighted benchmark. While this dynamic plays out, investors have paid little attention to the pond QSV fishes in, small and mid-cap equities, where the returns were quite different, and negative during the quarter. Each sector of the Russell 2000 Value index delivered losses in Q2, with Utilities (supported by the prospects for data centers for the AI revolution?) only slightly in negative territory and Healthcare, where QSV finds an ample supply of quality businesses, suffering losses of more than 10%. Returns for mid-cap indexes were in similar,

negative, territory.

More information including since-inception performance for each QSV strategy may be found at www.qsvequity.com.

QSV Strategy Quarterly Performance

QSV Small Cap returned -3.76% and -3.84%, gross and net of fees, respectively, lagging the Russell 2000 Value Index return of -3.64% and the Russell 2000 Index return of -3.28%. Security selection in Healthcare helped performance, while an overweight in the sector detracted. Selection in Real Estate also aided performance. Selection in Industrials and Financials businesses detracted from returns.

QSV Small Cap Top Contributors

Napco Security Technologies Inc. (NSSC) shares rose nearly 30% supported by strong growth in revenues and gross margins in its business units. NSSC is a global provider and manufacturer of high-tech security products, including access control systems, door-locking products, intrusion and fire alarm systems and video surveillance products. The company is focused on doubling revenue within its recurring, high-margin Services business in the next 2-3 years and currently produces returns on invested capital of 17% while selling at a discount to our measure of intrinsic value.

Hawkins Inc. (HWKN), rose more than 18%, contributing to performance. HWKN is a leading provider of chemicals and ingredients sold through its industrial, water treatment and health and nutrition segments. The company has benefitted from fast growth in its high margin water treatment business which is expected to drive higher earnings and free cash flow growth as it represents a larger portion of the firm’s overall revenues. HWKN produces returns on invested capital of 13%.

QSV Small Cap Top Detractors

Shares of clinical research organization Fortrea Holdings (FTRE) dropped more than 40% during the quarter as the company fell short of analysts’ estimates of revenues and earnings and the company lowered its outlook. The company, spun out of LabCorp (LH) in 2023, benefits from offering tools and testing to the biotechnology and pharmaceutical industries that are highly scripted in law, regulation, and practice. QSV believes that it is not uncommon for a company to struggle initially post-spinoff and has confidence in the long-term outlook for FTRE. As a result, we added to our position on weakness in the share price.

Alamo Group (ALG) shares declined during the quarter as a five-week strike in one of its plants is expected to impact the quarter’s financial results. The manufacturer of agricultural and vegetation maintenance equipment settled the strike with a five-year contract that should remove the risk of labor disruption for some time. ALG operates as forty global brands in two key divisions: industrial equipment and vegetation management equipment. The company benefits from an extensive dealer network and leading market share. Sixty percent of its revenues come from state and municipal government contracts.

QSV Small Cap Portfolio Activity

Shares of Forward Air (FWRD) were sold after the company added debt for its Omni Logistics acquisition and, in our view, could not clearly define the mission for the combined business. PubMatic (PUBM) and Shutterstock (SSTK) were each sold for valuation reasons. Scotts Miracle-Gro (SMG) was sold as they continued to struggle with the exposure to the cannabis industry and the addition of debt, reducing our estimate of the company’s intrinsic value. Proceeds were invested in existing holdings as well as new holding Catalyst Pharmaceuticals(CPRX), a biopharmaceutical company focused on developing therapies for people with rare, debilitating neuromuscular and neurological diseases.

QSV Mid Cap returned -5.15% and -5.38%, gross and net of fees for the quarter, trailing the -3.40% return of the Russell Mid Cap Value Index and the Russell Mid Cap Index return of -3.35%. Security selection in Consumer Staples companies helped performance, as did company selection and an overweight to Information Technology companies. Selection in Financials detracted as did selection and an overweight to Healthcare.

QSV Mid Cap Top Contributors

Monolithic Power SystemsInc. (MPWR) was the leading contributor to performance in the quarter as the company delivered strong earnings growth and benefitted from the outlook for AI-related tailwinds. MPWR is a global provider of high-performance, semiconductor-based power solutions. As a “fabless” company – one that does not manufacture the chips used in its products – MPWR has profited from devoting more resources to chip design rather than capital expenditures, resulting in greater free cash flows, higher margins, and returns on invested capital of 22%.

Teradyne Inc. (TER), a provider of semiconductor chip testing equipment, also contributed to performance during the quarter as it beat earnings estimates and affirmed guidance. AI-related opportunities are contributing to current growth and an enhanced outlook while the company’s exposure to mobility produces headwinds due to lower demand. TER produces returns on invested capital of 26% and sells below our estimate of intrinsic value.

QSV Mid Cap Top Detractors

Fortrea Holdings (FTRE) was the leading detractor to performance during the quarter and is discussed above.

Lincoln Electric Holdings (LECO) detracted from performance during the quarter as the company saw softness in its quarterly revenues and lowered its full year earnings guidance. We see these as short-term issues for LECO, a trusted name in welding, cutting, and brazing products, with a leading global market share. While still in the commercialization phase, LECO is developing an EV charger business that represents an additional growth opportunity for the business. The company has raised its dividend for twenty-two years and produces returns on invested capital of 21%.

QSV Mid Cap Portfolio Activity

There were no total sales or purchases of positions during the quarter. QSV did add to its position in the clinical research organization Fortrea Holdings (FTRE) on weakness in its share price and made other trims and additions based upon valuation and our convictions in the fundamentals of the businesses.

QSV Select returned -4.40% and -4.62%, gross and net of fees, lagging the returns of the Russell 2500 Value and Russell 2500 Indexes of -4.31% and -4.27%, respectively. Select is a high conviction strategy that holds QSV’s best ideas from our Small Cap and Mid Cap strategies. Security selection was positive in Industrials. Selection and an overweight in Information Technology and Consumer Discretionary holdings also aided performance. Selection detracted from returns in Financials and Healthcare holdings.

QSV Select Top Contributors

Napco Security Technologies Inc. (NSSC) was the leading contributor to performance during the quarter and is discussed above.

Tyler Technologies Inc. (TYL) rose as its transition to Software as a Service, subscription revenues and earnings increased. TYL is the largest provider of enterprise software products focused solely on the public sector, with a focus on local governments where high switching costs stand as Tyler’s competitive advantage. The company has a 98% customer retention rate and incremental margins in its subscription business of over 70%. We continue to believe that TYL will benefit from increased government spending on infrastructure.

QSV Select Top Detractors

Fortrea Holdings (FTRE) was the leading detractor to performance of QSV Select during the quarter and is discussed above.

Vestis Corporation (VSTS) detracted from performance during the quarter. Formerly a division of Aramark, VSTS provides uniform services and workplace supplies to North American Customers ranging from small businesses to Fortune 500 companies. Business performance has been impacted by client retention dropping because of off-cycle price increases and sub-par results from the company’s sales team. We believe the company’s focus on improved service and sales productivity will get this performance back on track.

QSV Select Portfolio Activity

Limited trading was done in QSV Select during the quarter, with trims and additions made to address valuations and quality upgrades.

Our Focus on the Long Term

We believe that mid-year reflection is appropriate for investors including a close look at asset allocation. With the concentration of returns to-date in large cap equities, and specifically in a handful of companies, many portfolios are tilted in favor of those holdings. Unintended bets may exist where investors in both passive and active funds have stakes in the Magnificent 7 companies that have increased in size. Markets could be “different this time” but if the outperformance of the S&P 500 over the smaller companies in the Russell 2000 persists throughout 2024 it will cap a four consecutive year period of such outperformance, something that has not occurred since 1995-1998. Small and mid-cap value equities excelled in the years that followed that, while investors in large cap stocks endured the “lost decade” of returns. Compelling valuations currently exist in small and mid-cap businesses. Coupled with the possibility of lower inflation, lower interest rates, and potential tailwinds from deglobalization, we see a convincing case for allocating to quality small and mid-cap companies.

Disclaimer:

Returns are for the respective composites of QSV Equity Investors. Gross returns are calculated net of trading fees. Net returns are calculated net of trading fees and net of the firm’s management fee. All dividends are assumed to be reinvested. The returns of the QSV Small Cap strategy are compared to the historical performance of the Russell 2000 Indices as they are widely used benchmarks for small capitalization securities. The returns of the QSV Mid Cap strategy are compared to the historical performance of the Russell Midcap Indices as they are widely used benchmarks for mid capitalization securities. The returns of the QSV Select strategy are compared to the historical performance of the Russell 2500 Indices as they are widely used benchmarks for SMID capitalization securities. An investment with QSV Equity Investors should not be construed as an investment in a program that seeks to replicate, or correlate with, these indices. Market conditions vary between the QSV products and these indices. Furthermore, these indices do not include any transaction costs, management fees and other expenses, as do QSV products. Lastly, QSV may invest in securities and positions that are not included in these indices.

No client or potential client should assume that any information presented should be construed as personalized investment advice. Personalized investment advice can only be rendered after engagement of the firm for services, execution of the required documentation, and receipt of required disclosures. Investing carries risk of loss.

QSV Equity Investors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of the CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. To view a GIPS report, please visit www.qsvequity.com.

QSV Equity Investors, LLC is a registered investment advisor. For additional information about the firm and its professionals please visit the SEC’s website at www.adviserinfo.sec.gov.